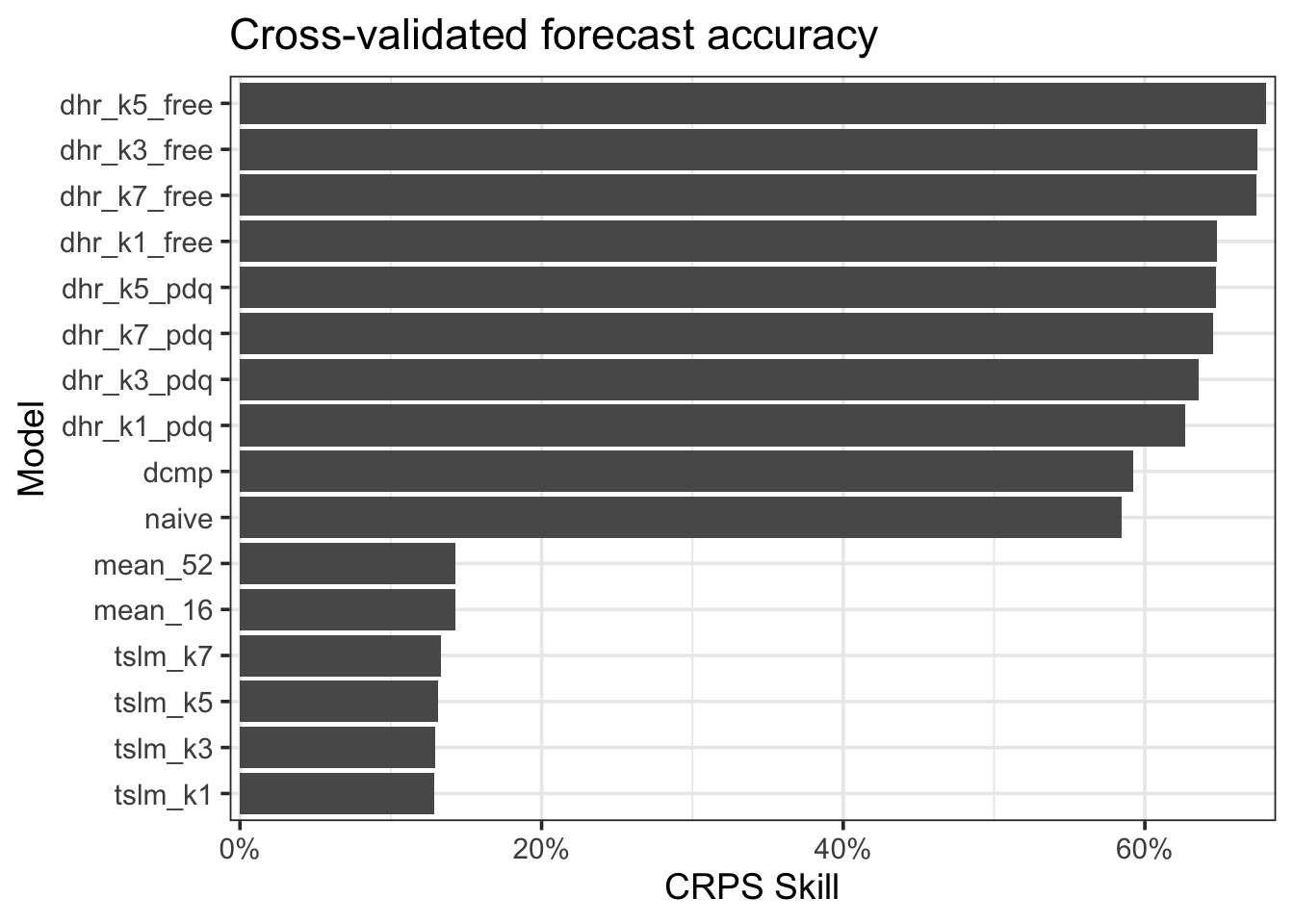

Rows: 8

Columns: 18

Key: .id, series [8]

$ .id <int> 1, 2, 3, 4, 5, 6, 7, 8

$ series <chr> "us_consumer_gas", "us_consumer_gas", "us_consumer_gas", "…

$ naive <model> [NAIVE], [NAIVE], [NAIVE], [NAIVE], [NAIVE], [NAIVE], [NAI…

$ dcmp <model> [STL decomposition model], [STL decomposition model], [S…

$ mean_16 <model> [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], …

$ mean_52 <model> [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], [MEAN], …

$ tslm_k1 <model> [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], …

$ tslm_k3 <model> [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], …

$ tslm_k5 <model> [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], …

$ tslm_k7 <model> [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], [TSLM], …

$ dhr_k1_pdq <model> [LM w/ ARIMA(2,1,2) errors], [LM w/ ARIMA(1,1,0) errors]…

$ dhr_k3_pdq <model> [LM w/ ARIMA(2,1,1) errors], [LM w/ ARIMA(0,1,1) errors]…

$ dhr_k5_pdq <model> [LM w/ ARIMA(1,1,0) errors], [LM w/ ARIMA(0,1,1) errors]…

$ dhr_k7_pdq <model> [LM w/ ARIMA(1,1,0) errors], [LM w/ ARIMA(0,1,1) errors]…

$ dhr_k1_free <model> [LM w/ ARIMA(4,1,1)(1,0,0)[52] errors], [LM w/ ARIMA(1,1…

$ dhr_k3_free <model> [LM w/ ARIMA(2,1,1)(1,0,0)[52] errors], [LM w/ ARIMA(0,1…

$ dhr_k5_free <model> [LM w/ ARIMA(1,1,0) errors], [LM w/ ARIMA(0,1,1) errors]…

$ dhr_k7_free <model> [LM w/ ARIMA(2,1,1)(1,0,0)[52] errors], [LM w/ ARIMA(0,1…